Financial technology. What does the future hold?

Forcing banks to bring their processes in line with the new realities, financial projects increase competition in the financial market which ultimately leads to the client’s side win.

What will be with this industry and its consumers in the future? Let’s come across the main trends that will determine the development of the financial industry in the coming years.

Contactless payments and IoT

“Smart” gadgets are getting more and more popular every day. Even now many of them are working in conjunction with each other. And in the next 5-7 years, it is expected to be a real boom of IoT development.

Connecting IoT with contactless payment technologies is a trend that is gaining momentum. The idea of embedding credit cards in things has already been realized. Today you can pay for your purchases with your smartphone and smartwatches in almost any store. In the near future, this feature may appear on other devices.

Thus, at the South by Southwest festival in Australia, Visa demonstrated a prototype of sunglasses with a contactless payment function. The glasses, called WaveShades, allowed festival visitors to pay for their purchases through POS-terminals. It is likely that in the future such “solvent” things will replace bank cards completely.

Customize

Suppliers implementing financial technologies and focus on the personalization of the services. In the research of The Boston Consulting Group, personalization is named one of the main global trends in retail banking development.

Sites, email and application content, paid media messages, discounts, sales notifications, product and service recommendations, as well as invoices and delivery reminders are personalized. And, of course, messages in social networks and chatbots.

Personalization becomes the cornerstone, it’s a long-playing trend that will remain upward for a very long time.

Digital banking and digital invoicing

Over the past few years, a whole class of new generation banks has grown in the world’s fully digital structures that rely only on remote interaction with customers. As a result – the growth of online payment and invoicing systems that accumulate tones of payments and process it with strict validation and in just a second.

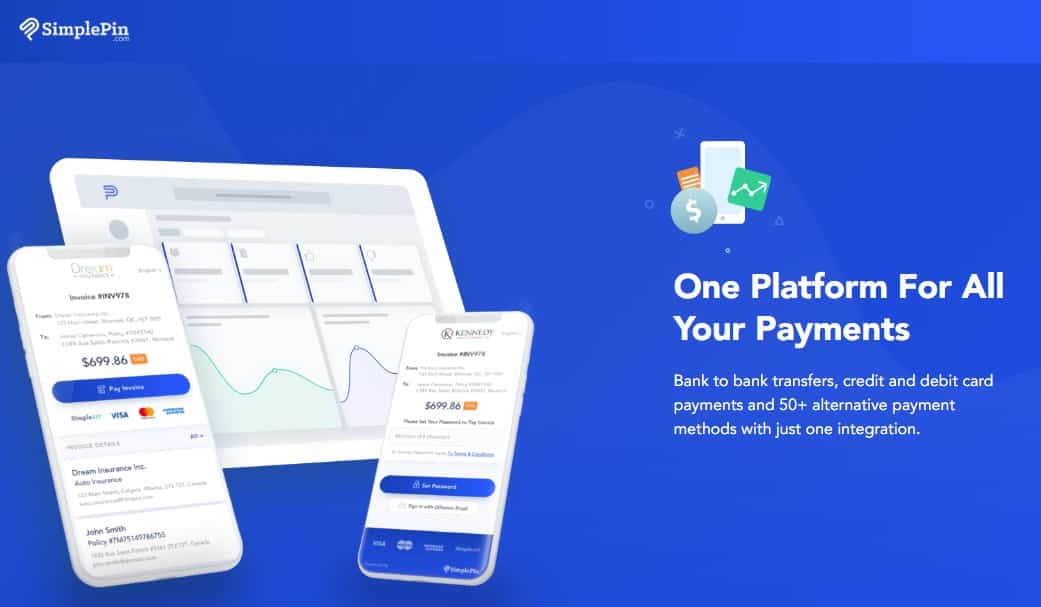

As an example – the project that we developed for the last 3 years – SimplePin – a digital invoicing platform focused on helping businesses collect their receivables with real-time payment methods online. SimplePin creates powerful payment and A/R automation solutions for businesses. Send customers invoices by email and they can pay online using SimplePin’s convenient, easy-to-use bank-to-bank payment gateway.

Blockchain

Blockchain is one of the most revolutionary technologies since the creation of the Internet. Last year, JPMorgan Chase patented a peer-to-peer payment network based on a blockchain that can be used for intra and interbank settlements. The patent application suggests using a distributed registry to process payments in real-time without having the need to rely on a third party to store a control copy of the information.

The Chinese public company Alibaba Group, which operates in the field of Internet commerce, has not been breathing smoothly towards the blockage for a long time. In the summer of 2018, Alibaba reported 90 patent applications for blockage development. Alibaba’s founder Jack Ma said that the company is going to allocate about $14 billion for this purpose.

Blockchain as a service.

The BaaS platform for entrepreneurs can be tested at alibabacloud.com. BaaS (Blockchain as a service) from Alibaba allows you to create an application for any needs of entrepreneurs and enjoy the delights of distributed registry technology. As described, the platform supports major open-source blockbusters such as Hyperledger Fabric and Enterprise Ethereum – Quorum. The platform promises to solve popular tasks: proof of origin, supply chain management, data sharing, protection of property rights.

In November 2019, The Wall Street Journal wrote about future collaboration between Google, Citigroup and Stanford University Credit Union. The companies are going to create co-branded Google Cache accounts based on Google Pay. Analysts have reacted to the news in different ways: some predict that the advertising giant, having gained access to a bank license, will become a threat to the financial giant, which will not be able to compete with it on price; others – believe that this is just the beginning of the era of Google experiments with the financial giant and the dangers are not expected yet.

In early 2020, the international payment system Visa bought Plaid financials for $5.3 billion. This open API platform allows technology companies to connect to users’ bank accounts more easily and quickly. Although Visa’s decision to pay 35 times more than Plaid earned last year surprised many, the corporation clearly knows what it is doing. Another fresh investment by Visa is the British start-up Currencycloud, which offers businesses a set of APIs for cross-border payments.

Hybrid products

Financial technologies, which originated as mono-products, are fighting for a leading role in the entire financial repertoire, which is available to the user. For this purpose, they create multiple solutions. Thus, the American MoneyLion, which has 5.7 million users, plans to add brokerage services, high yield savings accounts, and its own credit cards to the seven available products.

Innovative banks, expanding the digital product line, are becoming more universal and offer hybrid products such as investment cards and smart deposits such as Acorns or Robinhood.

Summary

Technologies Will Be At the Core of Financial Services Systems. The necessary technologies in the financial services industry have impacted almost all the business aspects in the years after 2010. These practices are gone, processes have become more transparent, and customers are opened to a great deal of personalization across products and services. According to this, in financial businesses:

- You should be ready for the “new normal” and to update your IT operations by using mobile technologies, IoT, or third-party vendors – there will not be other options.

- Build technology capabilities to get more intelligence about your clients’ needs( it matters when there is such a big market competition).

- Think about the future and make sure that you have access to the necessary talent and skills to execute and win. You could love new technologies or hate them, but if your decision and act will be quicker then your potential competitors – it could be ace up your sleeve.

Last Posts:

Typical software development teams’ structure and Agile engineering are often considered better than the old modes of software development because…

Could you spare me a couple of minutes? I have a really interesting idea!Okay, you have 1 minute. So, what…

We all have heard and continue witnessing extremely successful projects, “unicorns”. However, by studying startups which failed we can discover…

Previously, we have covered financials a startup should have and we mentioned a business plan several times. In the 12th…